Iran’s Tourism Industry: Where Civilizational Value Meets an Unfinished Market

Iran’s tourism industry is usually discussed through the language of attractions: ancient sites, religious cities, mountain landscapes, desert routes, islands, food, poetry, architecture, and hospitality. That language is not wrong, but it is insufficient for market analysis. Attractions explain why people may want to visit Iran. They do not explain where investment value is created.

The more useful question is different: why should tourism matter to Iran’s investment case at all?

The answer is that tourism in Iran is not merely a service sector. It is one of the clearest places where the country’s intrinsic assets meet its underdeveloped commercial systems. Iran has a deep base of historical, religious, geographic, medical, and cultural value. But much of that value is still poorly packaged, weakly verified, unevenly serviced, and difficult to transact.

That gap is the investment case.

The Starting Point: Iran Does Not Need to Invent Its Tourism Value

Many emerging tourism markets begin by manufacturing attention. They build resorts, create events, subsidize airlines, promote new districts, and try to persuade travelers that the destination is worth visiting.

Iran begins from a different position.

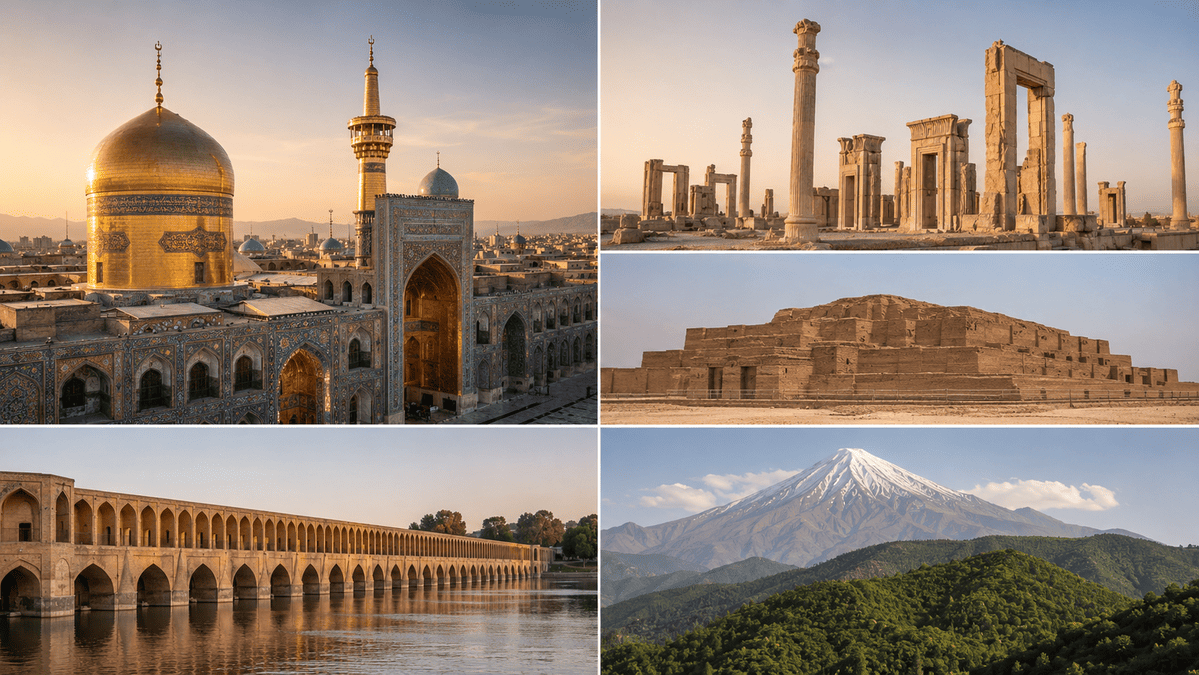

Isfahan, Shiraz, Yazd, Persepolis, Mashhad, Qom, Gilan, Kish, Qeshm, the Alborz mountains, the Zagros region, and the Persian Gulf coastline are not artificial demand generators. They already carry memory, identity, mobility, and recognition. Some draw international cultural interest. Some attract domestic families. Some serve pilgrims. Some support medical travel. Some sit on trade routes or coastal corridors.

This matters because capital can build hotels almost anywhere, but it cannot easily create historical depth, religious gravity, civilizational memory, or geographic variety. Those are place-based advantages. They make Iran different from a generic emerging market where tourism depends mainly on price, infrastructure, and marketing.

Iran’s problem is not absence of value. It is incomplete conversion of value into organized economic activity.

Why Tourism Is Strategically Relevant

Tourism is important because it can distribute economic activity across places that may otherwise sit outside the main investment map.

A petrochemical complex, mine, refinery, or industrial plant concentrates value in a specific asset. Tourism works differently. It spreads demand across accommodation, food, transport, retail, healthcare, local guides, cultural production, real estate, digital platforms, and municipal infrastructure. It can make a province commercially relevant even when that province is not a major industrial center.

This is why tourism belongs inside an Iran market-intelligence framework. It is not only about travelers. It is about how demand moves through provinces, roads, airports, clinics, shrines, heritage sites, islands, border cities, and domestic consumption patterns.

A serious tourism analysis therefore has to ask:

Where does demand already exist?

Where is the service layer weak?

Where does infrastructure limit conversion?

Where can trust be built?

Where can a fragmented local market become a structured business?

These questions are more useful than asking whether Iran has “potential.” It clearly does. The issue is whether that potential can be organized.

Iran Is Not One Tourism Market

The first strategic mistake is to treat Iranian tourism as a single sector.

The heritage route has one logic. Tehran, Isfahan, Shiraz, Yazd, Kashan, Kerman, Susa and Many others attract travelers through architecture, history, archaeology, craft, gardens, and urban memory. The commercial opportunity here is not just more hotel rooms. It is better interpretation, stronger route design, boutique hospitality, cultural retail, restoration-linked experiences, and higher-quality guiding.

Religious tourism has another logic. Mashhad and Qom are not occasional sightseeing destinations. They are recurring travel systems. Pilgrimage creates repeat demand, family travel, group movement, food consumption, retail activity, and accommodation pressure. The opportunity here is operational discipline: better mid-market hotels, transport coordination, family accommodation, multilingual services, crowd logistics, and trusted booking.

Medical tourism is different again. In Tehran, Shiraz, Mashhad, Isfahan, and Tabriz, the core asset is not scenery but medical capability, price advantage, specialist reputation, and proximity to neighboring markets. The missing layer is trust. Patients need verified doctors, transparent pricing, translation, recovery accommodation, airport handling, aftercare, and dispute resolution. In this segment, the service wrapper around treatment may become as valuable as the treatment itself.

Domestic leisure has its own structure. Gilan, Mazandaran, Ardabil, Kish, Qeshm, and mountain destinations are shaped by Iranian family travel, holiday peaks, villa rentals, food culture, road access, and seasonal behavior. This market is large, but informal. The opportunity is not to impose a foreign booking model mechanically. It is to professionalize domestic travel in a way that fits Iranian behavior.

The southern tourism market adds another layer. Hormozgan, Bushehr, Kish, Qeshm, Hormuz, and Chabahar sit between leisure, ports, free zones, retail, maritime access, and trade routes. The investment case here is selective. Free-zone status alone does not create value. Value appears where mobility, infrastructure, local identity, and service demand meet.

Each of these markets requires a different business model. That is why a generic tourism strategy for Iran will fail. The country has to be read province by province, corridor by corridor, and demand group by demand group.

The Real Product Is Infrastructure

In tourism, people often think the attraction is the product. In Iran, the more accurate view is that the journey is the product.

A shrine, island, historic square, desert town, or medical clinic may generate motivation. But the economic value depends on everything around it: airport access, road quality, hotel reliability, local transport, pricing transparency, language support, payment options, sanitation, emergency response, digital maps, booking rules, and customer protection.

This is where Iran’s tourism opportunity becomes clearer. Many destinations have enough underlying appeal. What they lack is dependable market infrastructure.

For example, a city with strong medical capability may still fail to capture foreign patient demand if the patient cannot verify the clinic, understand the price, arrange translation, trust the recovery facility, or manage the payment process. A northern town may attract large domestic flows but lose value through congestion, informal rentals, poor waste management, and weak service standards. A heritage route may be globally meaningful but commercially thin if interpretation, lodging, and transport remain fragmented.

This means investors should not look only for “beautiful places.” They should look for broken journeys.

Where the journey is broken, there may be room to build the business.

Challenges as Opportunity Maps

Iran’s tourism constraints are real: sanctions, payment friction, air connectivity, geopolitical risk, inconsistent service quality, regulatory complexity, weak data, water scarcity, environmental pressure, and logistics gaps.

But in an underbuilt market, constraints are not only warnings. They are also signals.

The trust gap points toward verification businesses. If travelers, patients, pilgrims, and domestic families cannot easily know which supplier is credible, then a platform or operator that verifies supply can capture value.

The logistics gap points toward route operators. If destinations are attractive but hard to navigate, then companies that organize transport, timing, local access, and support services can become essential.

The hospitality gap points toward mid-market operators. If luxury supply is limited and informal accommodation is inconsistent, then standardized, well-managed, family-friendly accommodation can serve real demand.

The medical-tourism gap points toward patient-service integrators. If hospitals exist but the patient journey is fragmented, then coordination becomes the business.

The data gap points toward intelligence products. If investors, operators, and public agencies lack reliable destination-level data, then mapping demand, supply, infrastructure, and constraints becomes valuable.

This is the correct way to read Iran’s tourism market. The challenge is not separate from the opportunity. In many cases, the challenge identifies the exact layer where investment can create value.

Where Investment Value Is Most Likely to Appear

The strongest opportunities are likely to be practical rather than glamorous.

Mid-market hospitality is one. Iran needs more reliable accommodation in cities where demand already exists but service quality is uneven. Mashhad, Qom, Shiraz, Isfahan, Yazd, Rasht, Ardabil, Tabriz, Kermanshah, Bandar Abbas, Qeshm, Kish, Kerman, Kashan, Hamedan, and Chabahar all deserve closer analysis. The best model may not be large luxury construction. It may be renovation, branded management, apartment-hotels, guesthouse standardization, and better operating systems.

Medical tourism coordination is another. Iran’s advantage in this segment depends on cost, reputation, and proximity, but the investable layer is trust. A strong operator can connect foreign patients to verified providers, manage the journey, and reduce uncertainty. This is especially relevant for demand from Iraq, Afghanistan, Azerbaijan, Oman, the Gulf, Central Asia, and the Iranian diaspora.

Religious travel services also matter. Mashhad and Qom already have recurring demand. The opportunity is to improve how that demand is served: accommodation, transport, food, family packages, multilingual support, medical add-ons, and retail. Pilgrimage is not a small niche. It is a durable mobility system.

Domestic tourism platforms are another major opportunity. Iranian families already travel extensively, but the market remains fragmented across informal rentals, scattered social media pages, local brokers, and inconsistent booking practices. A platform that can verify supply, manage disputes, handle payments, and understand local travel behavior could solve a real problem.

Province-based packaging may also become valuable. Iran is often presented as isolated sites, but the stronger commercial model is regional routing. Fars can be packaged through Shiraz, Persepolis, gardens, medical services, and cultural memory. Yazd can be built around desert architecture, caravanserais, Zoroastrian heritage, and slow travel. Gilan can connect food, forests, Caspian towns, rural stays, and domestic weekend demand. Hormozgan can link islands, ports, marine culture, winter travel, and free-zone services.

Finally, cultural retail is underdeveloped. Tourism creates demand for carpets, ceramics, textiles, saffron, pistachios, metalwork, jewelry, books, religious items, local foods, and design goods. Iran has the product culture. What is missing is modern packaging, provenance, distribution, retail format, and export-ready storytelling.

Why Iran Is Not Just Another Tourism Bet

The strategic question remains: why Iran?

The answer is not that Iran has fewer risks. It does not. The answer is that Iran’s tourism asset base is unusually hard to replicate.

A hotel can be built in many places. A clinic can be upgraded in many countries. A beach resort can be copied. A booking platform can be cloned. But the underlying reason people travel is not always transferable.

Persepolis is not transferable. Naqsh-e Jahan is not transferable. Mashhad’s pilgrimage economy is not transferable. Yazd’s urban fabric is not transferable. Gilan’s domestic food-and-leisure culture is not transferable. Iran’s position between the Persian Gulf, the Caspian, Central Asia, the Caucasus, Iraq, Afghanistan, Pakistan, and Turkey is not transferable.

This is what gives Iranian tourism its deeper investment relevance. The country’s tourism base is not built only on marketing. It is built on place.

That does not guarantee returns. It does, however, create a different kind of opportunity. Investors are not being asked to believe that demand can be invented. They are being asked to assess whether existing demand can be structured better.

Strategic Conclusion

Iran’s tourism industry is an unfinished market built on unusually strong underlying assets.

That is the core point.

The country has history, pilgrimage, medical capacity, domestic travel behavior, regional proximity, islands, mountains, deserts, forests, craft traditions, and cities with real cultural gravity. These assets give Iran a form of intrinsic investment value that many competing markets do not have.

But the commercial layer around those assets remains incomplete. Trust is weak. Data is limited. Hospitality is uneven. Booking is fragmented. Medical tourism is under-coordinated. Domestic travel is informal. Some destinations are physically reachable but operationally difficult. Environmental systems are under pressure.

This is where the opportunity sits.

The best tourism investments in Iran will not simply add more capacity. They will organize the market. They will make supply verifiable, journeys easier, service quality more predictable, destinations more legible, and local assets more commercially useful.

Iran’s tourism thesis is therefore not based on simple optimism. It is based on a structural gap: old assets, young systems.

For investors and operators, that gap is the point. The value is already there. The market has not yet learned how to fully capture it.