The Hard-Asset Lens: Which Assets Can Hold Value in an Inflationary Iran?

In inflationary economies, investors often move toward things they can touch. When cash loses purchasing power and financial numbers become harder to interpret, land, buildings, factories, warehouses, machinery, and inventory begin to feel more reliable than money. Iran has lived with this logic for years. For many domestic investors, physical assets are not only investment choices; they are defensive tools against the erosion of the rial.

Yet for a foreign investor, the question cannot stop at whether an asset is physical. The more important question is whether that asset can preserve usable value after ownership, liquidity, location, infrastructure, regulation, and exit are tested.

Hard assets are not automatically safe assets. A land parcel with unclear title is not a hedge. A factory without reliable utilities or working capital is not a platform. A warehouse in the wrong location is only a building. Agricultural land without water is not a productive asset. A property that cannot be sold may rise on paper while trapping capital in practice.

The hard-asset lens is therefore not about buying anything tangible. It is about identifying which forms of physical value can survive inflation, currency pressure, and operational reality.

Why hard assets matter in Iran

Hard assets matter in Iran because inflation changes the way people think about value. When money loses trust, investors search for assets that are harder to reproduce. Land cannot be printed. A completed building cannot be devalued like cash. Industrial equipment, warehouses, and raw materials may become more expensive to replace as the currency weakens. Existing physical assets can therefore acquire defensive value, especially when replacement becomes difficult.

This is one reason Iran’s physical economy deserves close attention. A factory built years ago may sit on land and infrastructure that would be much more expensive to recreate today. A warehouse near a logistics corridor may become more important if trade expands. A parcel close to a port, industrial zone, border route, or growing city may hold strategic value beyond its current income. Even inventory can become valuable when imported goods, spare parts, or raw materials become harder to source.

But physical value can also mislead. Inflation may lift nominal prices without improving real liquidity. Owners may ask for higher prices because they fear currency depreciation, while actual buyers become fewer. A property may look stronger on paper, but its transaction depth may weaken. A factory may be expensive to replace, yet unable to operate profitably. Land may be scarce, but unusable without permits, roads, water, or electricity.

The useful distinction is not between cash and physical assets. It is between physical assets that preserve usable value and physical assets that only appear protective.

Real estate as a store of value

Real estate is the most familiar hard asset in Iran. Residential apartments, commercial units, offices, villas, retail spaces, and mixed-use buildings have long served as stores of value for domestic capital. The appeal is clear: property is tangible, socially trusted, and historically associated with wealth preservation.

But Iranian real estate is not one market. Tehran is different from northern resort areas. Industrial cities behave differently from religious tourism centers. A commercial unit in a saturated retail district is not comparable to a warehouse near a transport route. A half-finished project carries a different risk profile from a fully titled, income-generating property.

The first question is whether the asset has real economic use. A property that generates reliable rent has a clearer value base than one that depends only on future appreciation. In inflationary markets, many investors focus on capital gains, but rental demand reveals whether the asset is still connected to purchasing power and productive use.

The second question is liquidity. Asking prices can rise even when transactions slow. This is common when sellers adjust expectations to inflation but buyers cannot keep up. In such a market, quoted value and realizable value can diverge. For a foreign investor, the ability to exit matters as much as the possibility of price appreciation.

Location also needs to be tested beyond slogans. Many properties are sold through narratives of future growth, new infrastructure, tourism demand, redevelopment, or scarcity. Some of these narratives are valid. Others are speculative. The investor needs evidence: access, buyer depth, zoning, nearby projects, local income levels, traffic patterns, and comparable transactions.

Real estate can preserve value in Iran when it combines clear ownership, real demand, usable location, income potential or buyer depth, and a credible exit path. Without those conditions, it may be more psychological comfort than investment protection.

Land: the asset beneath the asset

Land is often the most powerful hard asset because it sits beneath every other form of physical value. Urban land, industrial land, agricultural land, coastal land, and land near logistics corridors can each hold value for different reasons. But land is also one of the easiest assets to misunderstand.

Urban land may benefit from density, redevelopment potential, scarcity, and future construction demand. Its value, however, depends on zoning, municipal rules, permits, infrastructure access, and buyer affordability. Industrial land may become valuable near markets, ports, suppliers, labor pools, and transport routes, but only if utilities and operating permissions can support real activity. Coastal land may look strategic, especially near trade routes or tourism areas, yet development rights, environmental restrictions, ownership clarity, and infrastructure are decisive.

Agricultural land requires even more caution. In Iran, land without reliable water can lose much of its economic meaning. Soil quality, crop suitability, legal water access, local labor, cold chain, and market connection matter more than surface area. A large plot with weak water access is not necessarily a store of value; it may be a stranded claim on a resource under pressure.

Land near corridors, ports, borders, or industrial zones can be attractive when it benefits from actual movement of goods, labor, and capital. Proximity alone, however, is not enough. The investor must know what the land can legally become, what infrastructure it needs, who controls the approvals, how much development will cost, and who the final user or buyer might be.

This is the right way to view land in Iran: not as a passive object, but as an option on future use. Its value depends on what can realistically be unlocked.

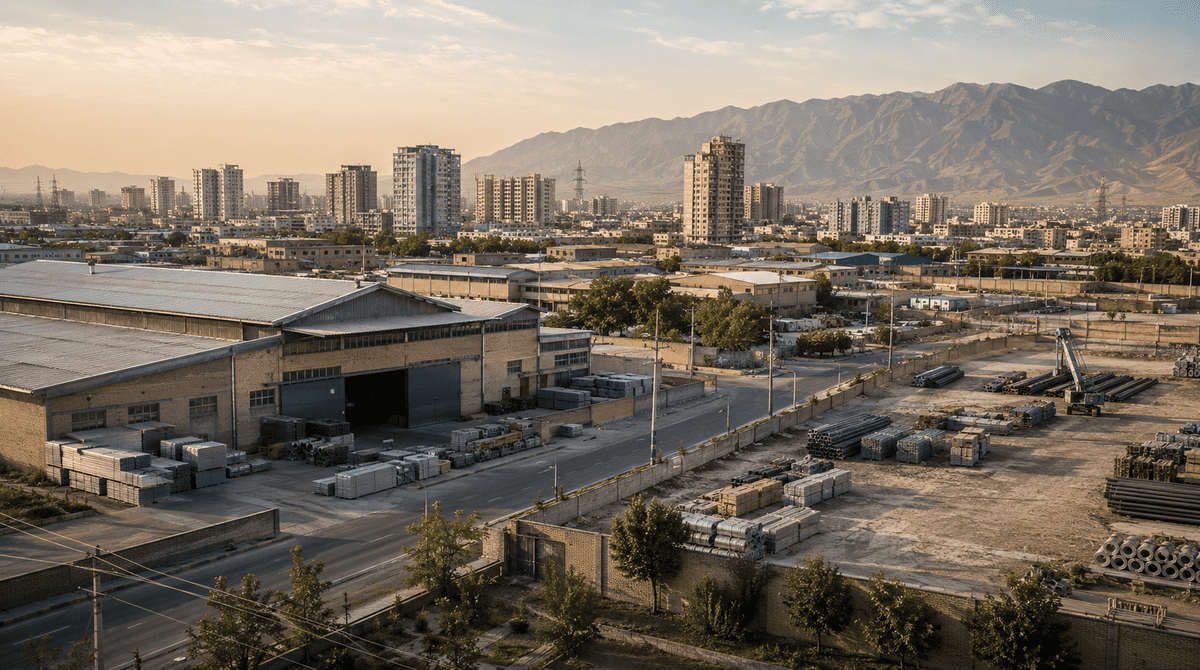

Industrial property

Industrial property is a more complex hard-asset category because it combines physical value with operating value. A factory, warehouse, cold storage facility, industrial yard, or ready-to-use production unit may preserve value through its land and structures, but it may also generate income if the operating base is intact.

A factory is not merely a building. It includes machinery, permits, utility access, labor, suppliers, customers, maintenance history, environmental obligations, safety requirements, and working capital. If these elements are weak, the physical shell may be worth far less than the headline valuation suggests.

Warehouses and logistics assets follow the same principle. Their value is shaped by location, truck access, loading capacity, security, proximity to customers, road connections, and demand from distributors or manufacturers. Cold storage facilities add another layer: electricity reliability, refrigeration maintenance, food and agriculture flows, customer contracts, and operating discipline.

Industrial assets can be attractive in Iran because replacement is often difficult. Recreating a licensed, connected, operational industrial site may require time, permits, imported components, construction, financing, and local relationships. Existing assets can therefore trade below replacement cost when owners are distressed or capital is scarce.

But the same assets can hide serious problems. Unpaid debts, tax issues, labor claims, environmental obligations, obsolete machinery, unclear permits, bank encumbrances, and supplier disputes can all sit behind a seemingly attractive price. The investor needs to understand why the asset is available and whether its discount reflects opportunity or unresolved liability.

A useful test is to value industrial property through three linked questions: what would it cost to replace, what can it actually produce or store, and how clean is the legal and financial position? If those answers align, the asset may have real defensive value. If not, the physical discount may be deserved.

Agricultural land and resource risk

Agricultural land is often presented as a natural inflation hedge because food demand is persistent. In Iran, that assumption is incomplete. Agricultural value is inseparable from water, climate, crop economics, and market access.

Water is the core issue. Without secure and lawful access to water, agricultural land may have limited real value regardless of its nominal price. Groundwater stress, changing rainfall patterns, competition between urban, industrial, and agricultural users, and rising operating costs can alter the economics of a farm quickly.

Crop choice also matters. A product may be valuable in one region and uneconomic in another. Export potential may exist, but certification, packaging, cold chain, transport, and buyer consistency determine whether that potential becomes revenue. Domestic demand may be stable, but price controls, intermediaries, and logistics costs can reduce margins.

For this reason, agricultural land should be assessed as a production system rather than a plot. The investor needs to understand water rights, soil, crop suitability, local labor, storage, processing, transport, buyer channels, and operational management. If those pieces are not present, the land may not function as a store of value.

Inventory as physical value

Inventory deserves a place in the hard-asset discussion because in inflationary economies it can become a form of short-term protection. For manufacturers, distributors, traders, healthcare suppliers, repair businesses, and industrial operators, the right inventory can preserve value when replacement costs rise.

This is especially true for imported components, spare parts, raw materials, packaging, metals, chemicals, construction materials, medical supplies, and essential food inputs. When currency weakens or imports become more expensive, existing stock may gain replacement value.

But inventory is a more fragile hard asset than land or property. It can expire, become obsolete, require costly storage, face regulation, or lose demand. It may rise in accounting value while becoming harder to sell. It can also trap working capital if the business misjudges demand.

Inventory protects value only when it is essential, liquid, hard to replace, and supported by broad buyer demand. For some businesses in Iran, disciplined inventory management may be more valuable than owning property. The right stock at the right time can protect margins; the wrong stock can freeze capital.

When hard assets are not safe

The main error investors make in inflationary markets is assuming that tangible assets are automatically safer than financial assets. In Iran, that assumption can be expensive.

Unclear ownership is the most serious risk. Disputed title, incomplete documentation, inheritance claims, informal arrangements, unclear boundaries, partner-held ownership, mortgages, or hidden encumbrances can turn a physical asset into a legal problem.

Liquidity is the second risk. Large properties, specialized equipment, agricultural land, luxury units, and minority stakes in asset-heavy companies may all be difficult to sell under stress. An asset that cannot be converted into cash or transferred to a real buyer may preserve local status but not investor value.

Pricing is another trap. Inflation can make sellers anchor to replacement fantasies rather than transaction reality. An asking price may reflect fear of currency loss more than market demand.

Permits and utilities are equally important. Land without the right zoning, a factory without operating approvals, a warehouse without safety clearance, or a project without municipal permissions should not be valued as if it were ready for use. Water, electricity, gas, roads, sewage, and telecommunications can determine whether an asset is operational.

Foreign investors also need an exit view from the beginning. If proceeds cannot be sold, converted, transferred, reinvested, or otherwise realized, the asset may preserve local value while failing the investor’s return test.

A hard asset becomes safe only when the legal, operational, and liquidity conditions support the physical value.

How investors should evaluate hard assets

A serious hard-asset review in Iran should begin with replacement cost, but it should not end there. Replacement cost asks what it would take to recreate the asset today: land acquisition, construction, machinery, permits, infrastructure, imported components, financing, time, and local execution. If the asset can be bought below credible replacement cost, there may be value.

The next layer is legal title. Ownership must be independently verified, including liens, disputes, claims, mortgages, inherited rights, partner arrangements, and transfer restrictions. For foreign investors, the legal structure of ownership is part of the asset itself.

Location should then be tested economically. A location is valuable if it reduces cost, increases demand, improves logistics, supports labor access, or creates a better exit. Describing a site as strategic is not enough. The logic has to be specific.

Liquidity determines whether physical value can become usable value. The investor should know who could buy or rent the asset later, how deep that buyer pool is, and how long exit might take under normal and stressed conditions.

Operating utility is the next filter. If the asset is meant to produce, store, host, rent, or distribute something, it needs the infrastructure and permissions to do so. Otherwise, the valuation should reflect speculation rather than operating value.

Finally, the investor must connect the asset to an exit path. Sale, rental income, operating cash flow, sale to a strategic buyer, reinvestment inside Iran, or partnership transfer each imply a different risk profile. The exit route should be understood before entry, not after problems appear.

Investor checklist

Before buying or financing a hard asset in Iran, investors should answer the following questions:

Is the title clear and independently verifiable?

Are there disputes, liens, debts, claims, or legal restrictions?

Does the asset produce income, or is it held only for value preservation?

If it produces income, is that income collectible and repeatable?

If it does not produce income, who is the likely future buyer?

Is there a real secondary market?

Does the asset have water, electricity, gas, road access, permits, and operating approvals?

Is the location valuable for a specific economic reason?

What is the replacement cost in today’s conditions?

Which exchange rate is being used to judge the price?

Can the investor legally own, control, lease, sell, or benefit from the asset?

How can capital exit?

Who is the local partner, and what do they actually control?

What could make the asset difficult or impossible to sell?

What to watch

Hard-asset values in Iran should be monitored through inflation, exchange rates, construction costs, rent trends, land-use rules, municipal policy, utility constraints, water scarcity, industrial-zone demand, logistics corridors, port activity, and credit conditions.

Public-company disclosures can also be useful. Construction, cement, steel, real estate, and industrial companies often reveal signals about material costs, land values, project delays, debt pressure, and sector margins. Property platforms and advertisements can show asking-price behavior, but they should be treated as market signals rather than verified transaction data.

The most reliable picture comes from triangulation: official data, market listings, legal checks, local interviews, transaction evidence, and physical inspection.

Inflation can make almost every physical asset look attractive for a period. But only some assets preserve real value after ownership, use, liquidity, and exit are tested.

That is the hard-asset lens.