The Rial Question: Will Currency Risk Erase the Upside in Iran?

Iran often looks cheap from the outside.

Industrial assets may appear underpriced. Labor may look inexpensive in dollar terms. Listed companies may trade at modest valuations. Land, factories, warehouses, consumer businesses, and export-linked companies can seem mispriced compared with regional markets.

But cheapness in Iran is never self-explanatory.

The first question is not whether an asset is cheap in rials. The real question is whether the opportunity still works when measured in dollars, euros, or dirhams.

That is the Rial Question.

For foreign investors, currency is not a separate item at the end of the risk section. It is the first translation layer. Every Iranian opportunity must pass through it: purchase price, revenue, costs, inflation, asset value, partner payments, working capital, and exit.

A project can make money in rials and still lose value in hard-currency terms. A company can grow revenue while merely keeping pace with inflation. A property can rise in local price but fail to protect dollar value. A factory can look cheap until imported machinery, spare parts, and working capital are priced correctly.

Currency risk can erase upside. But it can also explain why the upside exists.

The investor’s task is to distinguish between assets that are genuinely mispriced and assets that only look cheap because the currency lens is wrong.

Why currency comes first in Iran

Iran is priced locally in rials, but most foreign investors measure return in hard currency.

That creates the basic analytical gap.

Inside Iran, salaries, rents, many contracts, domestic sales, local taxes, and accounting figures are usually expressed in rials. Outside Iran, the investor thinks in dollars, euros, dirhams, or another hard-currency benchmark. The investment may operate in one monetary world while the investor evaluates it in another.

This affects every asset class.

A local business may report strong rial revenue growth. But if the rial weakens faster than revenue rises, the investor’s hard-currency return may be poor.

A land parcel may increase in local price. But if liquidity is weak, title is unclear, or the exit exchange rate is worse than the entry rate, the apparent gain may not be realizable.

A manufacturing business may benefit from cheap local labor. But if it depends on imported equipment, foreign raw materials, or hard-currency components, depreciation can damage margins.

An exporter may gain from a weaker rial if revenues are linked to foreign prices while costs remain local. But sanctions, settlement routes, export rules, and logistics can reduce that advantage.

This is why currency comes first. It decides how the opportunity is translated from local value into investor return.

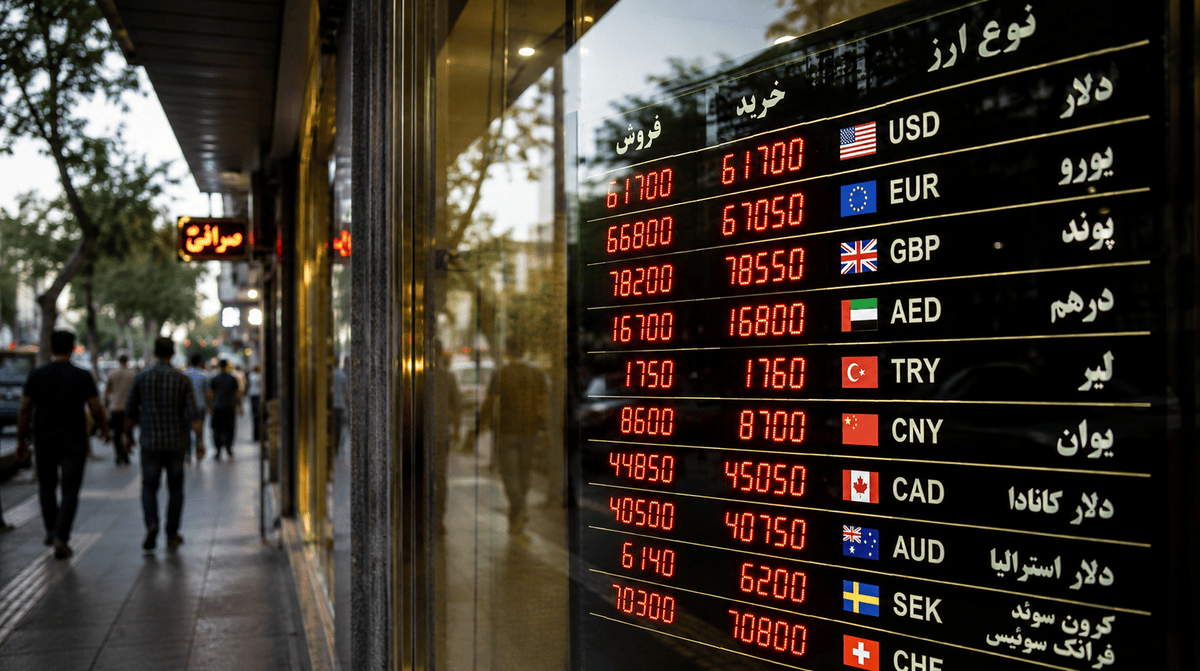

Official rates, market rates and distorted prices

The next problem is that Iran does not always have one useful exchange rate.

Different rates may exist for different purposes: official reporting, regulated trade, commercial allocation, market transactions, remittance, cash exchange, and operational settlement. The names and mechanisms may change over time, but the analytical problem remains the same.

An investment can look attractive or unattractive depending on which rate is used.

This creates a common mistake: the investor calculates the purchase price with one rate, estimates costs with another, assumes revenue using a third, and imagines exit using a fourth, often without noticing the inconsistency.

A serious valuation must separate these rates.

There is the rate used to bring capital in.

There is the rate used to buy the asset.

There is the rate that affects imports and replacement costs.

There is the rate reflected in local market behavior.

There is the rate available when capital needs to exit.

If these are not the same, the difference is not a technical detail. It is part of the investment risk.

For example, a company may look cheap using an official conversion rate but not cheap using the practical market rate. A factory may look profitable under accounting assumptions but less attractive once imported spare parts are priced at real replacement cost. A consumer business may show local growth but lose value when translated at the rate available to the investor.

The first discipline, therefore, is simple: every Iranian valuation must state its exchange-rate assumption.

Without that, the price is incomplete.

Inflation and the illusion of growth

After currency, the second translation problem is inflation.

In an inflationary economy, nominal growth can imitate real growth. Sales rise. Asset prices rise. wages rise. Inventory values rise. Land prices rise. But not all of this is economic progress. Sometimes it is only the local currency losing purchasing power.

This is especially important in Iran because many opportunities are first presented through local numbers.

A food company may show higher revenue because it raised prices, while real volume is flat or falling.

A property may be listed at a higher rial price, while the pool of real buyers is shrinking.

A retailer may report growth, but customers may be trading down to cheaper goods.

A manufacturer may hold inventory that rises in replacement value, but then struggle to finance the next production cycle.

A listed company may look more profitable, while its true margin is being squeezed by imported inputs, financing costs, or regulated pricing.

The investor has to separate three things:

Price increase.

Volume increase.

Real value increase.

These are not the same.

The most useful test is replacement cost. What would it cost to rebuild the asset today? What would it cost to import the same machinery? What would it cost to buy the land, secure permits, construct the facility, hire labor, and restart operations?

In Iran, old balance-sheet values can understate the value of real assets. But inflation can also create false confidence. A nominally expensive asset may still be operationally weak, illiquid, legally complex, or hard to exit.

The right question is not: “Has the price gone up?”

The right question is: “Has the asset preserved or increased hard-currency value after inflation, liquidity risk, and exit friction?”

Which assets can survive currency pressure?

Currency pressure does not affect all assets equally. The investor needs to classify assets by how they behave when the rial weakens.

1. Hard assets

Land, real estate, warehouses, industrial sites, factories, and physical infrastructure can protect value because they are tangible and difficult to recreate. In Iran, many domestic investors use them as inflation shelters.

But hard assets are not automatically safe.

A land asset needs clean title, proper zoning, real demand, access to roads, utilities, and a buyer base. A factory needs usable machinery, permits, workers, suppliers, and working capital. A warehouse needs location logic and tenant demand. A property needs liquidity, not just a quoted price.

Hard assets can protect value when they are useful, legally clean, and sellable.

2. Commodity-linked assets

Metals, petrochemicals, minerals, energy-linked products, gold-related markets, and certain agricultural goods are closer to global pricing logic. When the rial weakens, their local price may adjust because their value is tied to international benchmarks or replacement cost.

This can offer partial protection.

But it is not risk-free. Regulation, export restrictions, feedstock rules, sanctions, logistics, and payment settlement can all interfere with the theoretical currency benefit.

3. Export-oriented companies

Companies with export revenue can benefit when they earn in hard-currency-linked markets and pay part of their costs locally. This is why petrochemicals, metals, mining, and some industrial exporters deserve attention.

The key issue is whether export earnings can actually be realized, settled, and used.

A company may sell abroad, but the investor still needs to understand collection, sanctions exposure, transport, currency conversion, and repatriation.

4. Local-cost businesses

Some businesses benefit from Iran’s lower hard-currency cost base: engineering, software, technical services, manufacturing support, repair, design, and operational teams.

These are attractive when the output can be sold into higher-value markets or when local efficiency creates a defensible margin.

But the model must avoid imported-cost traps. Cheap labor does not compensate for expensive inputs if the business cannot pass costs to customers.

5. Import-dependent businesses

These are the most exposed.

If a company earns in rials but buys inputs in foreign currency, depreciation can destroy margins. This is especially dangerous in sectors with price controls, weak purchasing power, or slow regulatory approval for price increases.

A business with rial revenue and dollar costs needs unusually strong pricing power, inventory discipline, and working-capital management.

When currency risk creates opportunity

Currency pressure can create opportunity when it forces mispricing.

In markets with limited foreign participation, sanctions friction, weak transparency, and domestic liquidity cycles, investors often overreact or underprice certain assets. Some assets are discounted because they are difficult to understand, not because they lack value.

Opportunity appears when three conditions meet.

First, the asset is priced in distressed local terms.

Second, the underlying value is linked to something more durable: land, replacement cost, export earnings, strategic location, commodity exposure, or essential demand.

Third, the investor can control, operate, protect, and eventually exit the asset.

This is where Iran can become interesting.

A factory may be undervalued because local owners lack capital, while its land, permits, machinery, and workforce would be expensive to recreate.

A logistics asset may be mispriced because the market underestimates its location near a port, border, or industrial corridor.

An exporter may trade at a discount because investors fear currency and sanctions risk, while its actual revenue base is more resilient than domestic companies.

A consumer business may look weak in premium categories but strong in essential goods, repairs, discount retail, or substitution-driven demand.

A technology or service company may benefit from a skilled local workforce priced far below regional alternatives.

In these cases, the weak rial is not just a danger. It is part of the reason the asset may be available at an asymmetric price.

But the opportunity only exists if the discount can be converted into real ownership, cash flow, or exit value.

Cheap without control is not cheap.

Cheap without liquidity is not cheap.

Cheap without legal clarity is not cheap.

Cheap without exit is not a return.

When currency risk destroys opportunity

Currency risk destroys opportunity when the business model cannot absorb depreciation.

The most obvious case is a company with local revenue and foreign costs. A medical distributor, electronics importer, machinery-dependent manufacturer, or consumer-goods business may look attractive until the next currency move raises input costs faster than the company can raise prices.

The second case is regulated pricing. If a company cannot adjust prices freely, inflation and depreciation can turn growth into margin compression.

The third case is trapped capital. An asset may rise in rial terms, but if the investor cannot convert or transfer proceeds, the return may remain locked inside the local system.

The fourth case is weak contract design. In a volatile currency environment, contracts that do not define payment currency, adjustment mechanisms, settlement timing, penalties, and dispute resolution can break under pressure.

The fifth case is working-capital shock. After depreciation, the same business may need much more rial liquidity to buy inventory, import parts, or continue production. A profitable company can become cash-starved.

The sixth case is false liquidity. Real estate, private company stakes, industrial equipment, and minority holdings may show attractive paper value but become difficult to sell during stress.

These are not separate risks. They are the ways currency enters the operating model.

The investor must therefore ask: where exactly does currency pressure hit this opportunity?

At purchase? At revenue? At costs? At debt? At inventory? At contracts? At exit?

Only after locating the exposure can the risk be priced.

The practical return framework

A foreign investor should not evaluate Iran with a single return number.

The analysis should move through five layers.

1. Nominal rial return

This is the local accounting return. It shows what happens inside Iran before inflation and currency adjustment. It is useful, but incomplete.

2. Real rial return

This adjusts for inflation. It asks whether the investment is gaining purchasing power within Iran.

3. Hard-currency return

This translates the result into dollars, euros, or dirhams. For most foreign investors, this is the central benchmark.

4. Exit-adjusted return

This asks whether the return can actually be converted, transferred, reinvested, or realized. A return that cannot exit is not equivalent to a return that can.

5. Risk-adjusted return

This includes legal structure, sanctions exposure, partner risk, liquidity, tax, regulation, contract enforcement, and political or operational uncertainty.

An opportunity may look strong at the first layer and weak at the fourth. Another may look ordinary in nominal terms but strong after replacement cost and hard-currency protection are properly understood.

The conclusion should not be based on whether Iran is “cheap.” It should be based on whether the asset survives all five layers.

Investor checklist

Before investing in Iran, the currency question should be made explicit.

Which exchange rate is being used?

Is the valuation based on an official rate, market rate, remittance rate, or practical settlement rate?

Does the same rate apply to entry, operations, imports, revenues, and exit?

What currency drives revenue?

Is revenue purely local?

Is it export-linked?

Is it commodity-linked?

Can prices adjust when the rial weakens?

What currency drives costs?

Are inputs local or imported?

Does the business need foreign machinery, software, raw materials, spare parts, licenses, or financing?

Can it keep operating after depreciation?

Is growth real or nominal?

Are volumes rising?

Are margins stable?

Is the business gaining purchasing power or only reporting inflation-driven revenue growth?

Does the asset protect value?

Is it scarce, useful, legally clean, and liquid?

What is its replacement cost?

Can it be sold under stress?

Can capital exit?

How does money enter?

How does money leave?

What happens if exit is delayed?

What exchange rate applies at exit?

What is the stress scenario?

If the rial weakens further, does the thesis survive?

If inflation accelerates, does the asset protect value?

If consumers trade down, does demand remain?

If liquidity disappears, can the investor still realize value?

What to watch

The rial question is not answered once. It must be monitored continuously.

Investors should watch exchange-rate gaps, inflation data, gold and coin prices, real estate behavior, commodity prices, import costs, export settlement rules, central-bank policy, and signs of pressure in consumer purchasing power.

They should also compare how different assets respond. Exporters, commodity producers, land, housing, gold, consumer staples, import-dependent companies, banks, and industrial firms each react differently to currency stress.

The strongest opportunities in Iran will not simply be the cheapest assets in rial terms. They will be the assets where the investor can understand the currency exposure, verify real value, protect against inflation, structure cash flows, and define a credible exit.

The rial can erase the upside.

But when understood correctly, it can also reveal where the upside is real.