Iran’s Hidden B2B Market: The Demand Created by Friction

The easiest way to misunderstand Iran is to look only at the consumer market.

Consumer demand is visible. It appears in food, healthcare, education, retail, travel, digital services, and everyday household spending. It is easy to describe and easy to imagine. A large population needs products and services, so the consumer story feels immediately attractive.

But some of Iran’s most important demand is less visible. It sits behind the storefront, behind the factory gate, behind the customs desk, behind the mine, behind the warehouse, behind the hospital procurement office, behind the workshop trying to keep old machinery running for another year.

This is enterprise demand: the demand created by companies that need to operate inside a difficult environment.

In Iran, the most investable B2B demand is not created only by normal expansion. It is created by friction. Supply chains are harder than they should be. Machinery ages faster than it can be replaced. Imported inputs are expensive or uncertain. Power reliability affects production. Logistics are fragmented. Business data is incomplete. Compliance is complex. Currency volatility changes procurement decisions. Firms are forced to improvise.

That friction is not just a problem. It is a market signal.

Where businesses keep losing time, money, reliability, or capacity, demand begins to form. The question for investors is whether that demand is strong enough, repeated enough, and painful enough to support a business.

The Productive Economy Has a Different Kind of Demand

Consumer markets are driven by households. Enterprise markets are driven by operating necessity.

A household may delay a discretionary purchase. A factory cannot ignore a broken machine. A logistics operator cannot ignore route delays. A food processor cannot ignore cold-chain failure. A mine cannot ignore spare-parts shortages. A hospital cannot ignore consumables. A construction firm cannot ignore material supply. A retailer cannot ignore inventory distortion when inflation moves faster than planning.

This gives enterprise demand a different character. It is less emotional than consumer demand and often less visible from the outside, but it is tied more directly to business continuity.

The first analytical mistake is to treat B2B demand as a sign of healthy expansion only. In Iran, demand often appears because companies are defending their existing capacity. They are not always buying to grow. Many are buying to keep production alive, reduce downtime, replace imports, improve control, or survive volatility.

That matters because survival demand can be more persistent than growth demand. A company may cut advertising, delay renovation, or postpone new hiring. But it still needs parts, fuel, packaging, accounting, logistics, maintenance, permits, payment handling, and reliable suppliers.

This is where Iran’s hidden B2B market begins.

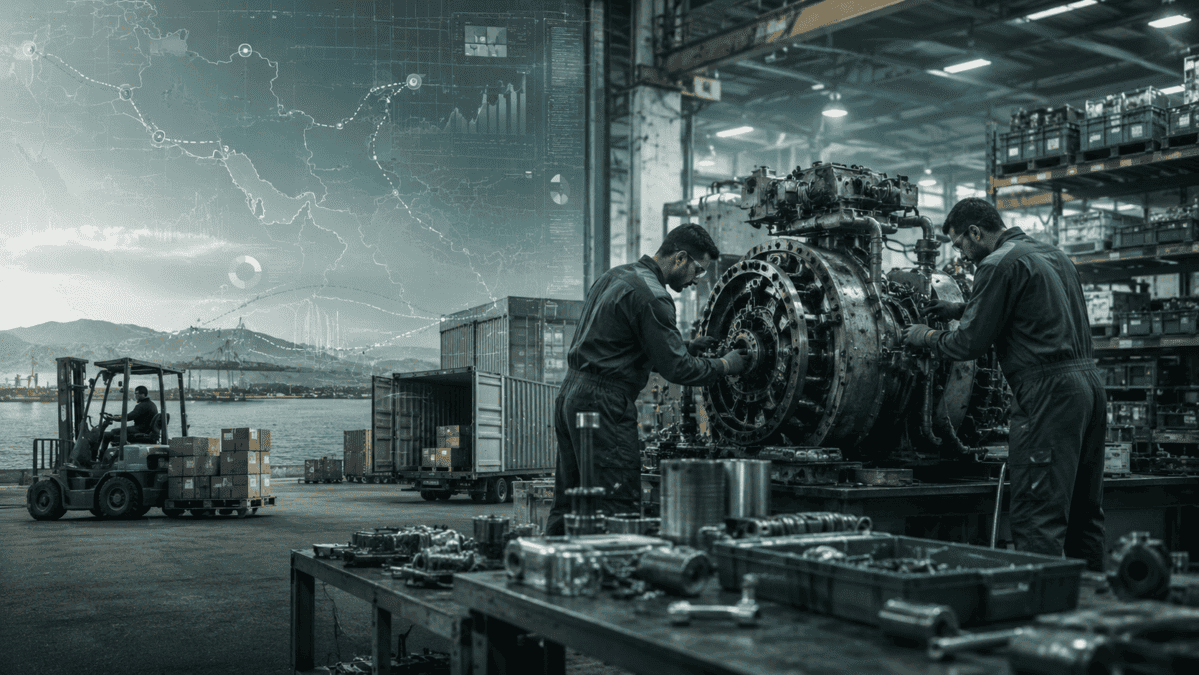

Friction One: Aging Equipment and the Maintenance Economy

Iran has a large base of industrial and productive assets: factories, workshops, mines, farms, processing plants, transport fleets, construction equipment, energy-related facilities, and logistics sites. Much of this productive capacity depends on machinery that requires constant repair, adaptation, and parts sourcing.

In a normal market, old equipment is replaced on a predictable cycle. In Iran, replacement is often delayed. Currency pressure raises the cost of imported machinery. Sanctions complicate supplier access. Documentation, payment channels, insurance, and after-sales support can become difficult. Some firms cannot justify new imports, so they extend the life of existing machines.

This creates a maintenance economy.

The opportunity is not only in selling new machines. It may be in spare parts, repair networks, diagnostics, retrofitting, second-hand machinery, local fabrication, technical training, reverse engineering, maintenance software, and supplier verification.

For investors, the point is not simply that “machinery demand exists.” The sharper point is that a constrained replacement cycle creates recurring demand around the installed base. The more difficult it is to replace equipment, the more valuable it becomes to maintain, adapt, and keep that equipment working.

The strongest demand will not be evenly distributed. It will cluster around industrial provinces, mining regions, construction-material hubs, logistics routes, food-processing centers, and ports. A machinery service business without geography is just an idea. A machinery service business placed near real productive clusters becomes much more serious.

Friction Two: Import Uncertainty and Local Substitution

Import dependence is one of the main forces behind enterprise demand in Iran.

Many sectors rely on imported machinery, components, chemicals, packaging, medical equipment, technology, spare parts, raw materials, or specialized tools. When imports become uncertain, expensive, delayed, or administratively complex, businesses do not simply stop needing those inputs. They search for substitutes.

This is where local production, supplier discovery, procurement intelligence, and quality verification become valuable.

An Iranian manufacturer may need to know which inputs can be sourced domestically, which must still be imported, which local suppliers are credible, and which substitutions will damage product quality. A hospital may need reliable consumables. A food company may need packaging that protects shelf life. A construction company may need alternative materials. A mine may need parts that can survive harsh operating conditions.

The opportunity is often in the middle layer between demand and supply.

Not every supplier is reliable. Not every local substitute works. Not every imported input can be replaced. This creates room for businesses that can verify suppliers, aggregate demand, improve procurement, certify quality, manage inventories, or connect buyers to credible producers.

In this sense, import friction does not only create manufacturing demand. It creates information demand. Companies need to know what can be bought, from whom, at what quality, under what terms, and with what delivery risk.

That is a B2B market.

Friction Three: Energy Reliability as an Operating Cost

Energy is not just a macro issue. For enterprises, it is a production variable.

Power interruptions, fuel access, energy pricing, cooling needs, seasonal pressure, and grid constraints can affect factories, cold storage, hospitals, farms, mines, workshops, warehouses, data-related services, and retail operations. When reliability falls, companies do not only lose electricity. They lose time, product quality, machine life, delivery discipline, and customer trust.

This creates enterprise demand for reliability.

Backup power, generators, solar systems, batteries, energy audits, efficiency upgrades, monitoring tools, cooling systems, load management, maintenance contracts, and operational redesign can all become relevant. The same logic applies to water in water-sensitive sectors: agriculture, food processing, mining, chemicals, construction, and industrial production.

The important distinction is that reliability services are not abstract sustainability products. In Iran, they are often business-continuity products.

A factory does not need an energy solution because it wants to look modern. It needs one if downtime threatens production. A cold-storage operator does not need monitoring as a luxury. It needs it if spoilage destroys margins. A farm does not need water efficiency because it is fashionable. It needs it if water stress makes the business fragile.

Investable demand appears when unreliability creates measurable loss.

Friction Four: Logistics Fragmentation

Iran’s geography is one of its strongest strategic advantages, but geography does not move goods by itself.

Goods still need ports, roads, rail, trucks, customs clearance, warehouses, insurance, documentation, packaging, storage, cold chain, regional distributors, and trusted operators. A route may look strong on a map and still be weak in execution.

This gap between geographic potential and operational reliability is one of the clearest sources of enterprise demand.

Manufacturers need inputs delivered on time. Importers need customs clarity. Exporters need predictable routes. Retailers need regional distribution. Food companies need cold chain. Construction firms need materials moved across provinces. Mines need heavy logistics. Hospitals need reliable supply.

The demand is not only for transport capacity. It is for coordination.

That includes route intelligence, warehousing, freight management, customs support, inventory planning, temperature-controlled logistics, fleet maintenance, cargo tracking, documentation services, and regional distribution partnerships.

For investors, logistics should be read as an enabling market. It does not only serve trade; it determines whether other sectors can function. A food business without cold chain is limited. A mining asset without transport is trapped. A retailer without inventory control loses margin. A factory without input reliability cannot plan production.

The investable question is simple: where does movement fail often enough that someone will pay to make it more reliable?

Friction Five: Weak Operational Data

Many Iranian businesses operate with fragmented data.

Information may sit in spreadsheets, notebooks, relationships, memory, disconnected software, messaging apps, paper invoices, and informal supplier networks. This can work when a business is small and stable. It becomes dangerous when inflation, currency pressure, supplier uncertainty, inventory swings, and receivable delays all happen at the same time.

In that environment, operational visibility becomes valuable.

Companies need to know what they have, what they owe, what is delayed, which customer is profitable, which supplier is unreliable, which product line is losing margin, which warehouse is overstocked, which invoice is unpaid, and which route is causing leakage.

This creates demand for practical enterprise software. Not necessarily sophisticated enterprise systems at the beginning. Often the opportunity is in simple, localized tools that solve immediate problems:

Inventory control.

Procurement tracking.

Receivables management.

Maintenance logs.

Fleet monitoring.

Warehouse visibility.

Supplier records.

Production planning.

Energy monitoring.

Basic business intelligence.

The mistake is to think of software only as a technology sector. In Iran’s enterprise market, software is a control mechanism. It helps firms defend margin in an unstable operating environment.

The best software opportunities will not begin with abstract digital transformation language. They will begin with a specific operational pain that companies already recognize.

Where the Real Opportunity Sits

The most attractive enterprise opportunities usually sit at the intersection of three forces: productive activity, constraint, and repeat demand.

A mining district with equipment problems creates one kind of opportunity.

A food-processing region with packaging and cold-chain gaps creates another.

A port province with customs and warehousing demand creates another.

A manufacturing belt with aging machinery and supplier fragmentation creates another.

A large urban market with retailers, clinics, schools, and service businesses creates another.

This is why enterprise demand must be mapped by sector and province together. National-level analysis is too blunt. The same B2B service may be valuable in one cluster and irrelevant in another.

Tehran and Alborz matter for headquarters, distribution, finance, software, services, and consumer-facing enterprise infrastructure. Isfahan, Markazi, Qazvin, Yazd, East Azerbaijan, and Kerman matter for manufacturing, machinery, mining, and industrial depth. Khuzestan, Bushehr, and Hormozgan matter for energy, petrochemicals, ports, trade, logistics, and heavy industry. Razavi Khorasan and border provinces matter for regional trade, food systems, transit, and cross-border commerce.

Enterprise demand is not floating in the economy. It is attached to places.

Why Need Is Not Enough

Iran has many business needs. That does not mean every need is investable.

This distinction is essential.

A company may need better software but lack budget. A factory may need new machinery but be unable to import it. A logistics operator may need tracking systems but resist formalization. A supplier may need quality improvement but lack incentive. A buyer may want better service but delay payment. A market may be large but too fragmented to serve profitably.

Investable demand requires more than pain. It requires payment capacity, repeat purchase, a clear buyer, feasible delivery, and a measurable business case.

The strongest B2B opportunities usually meet several tests:

The problem causes direct financial loss.

The buyer already understands the pain.

The solution can be localized.

The sales process is not impossibly slow.

The product or service reduces cost, downtime, risk, or uncertainty.

The need repeats over time.

The provider can build trust through execution, not only branding.

This is where many market-entry ideas fail. They identify a real problem but not a viable buyer. Hormuz should not map problems alone. It should map problems that can become transactions.

How Investors Should Screen Enterprise Demand

An investor looking at Iran’s B2B market should begin with friction, not sector labels.

Instead of asking, “Is manufacturing attractive?” ask: which manufacturing processes are repeatedly interrupted by input shortages, machinery failure, energy issues, logistics gaps, or weak data?

Instead of asking, “Is software attractive?” ask: which operational decisions are currently being made blindly, and who loses money because of that?

Instead of asking, “Is logistics attractive?” ask: where do delays, storage gaps, customs friction, or route uncertainty change the economics of trade?

Instead of asking, “Is machinery demand large?” ask: which installed equipment base is expensive to replace, critical to production, and underserved by maintenance networks?

This approach separates real demand from broad themes.

The investor is looking for bottlenecks that are painful, repeated, and close to cash flow. The closer the solution is to revenue protection, cost reduction, downtime prevention, or supply reliability, the stronger the opportunity.

The Hormuz View

Enterprise demand is one of the most important layers in the Hormuz graph because it reveals how the real economy actually functions.

It connects industries to suppliers, infrastructure to operating constraints, provinces to clusters, shortages to services, and investment theses to practical entry points. It also exposes where capital alone is not enough. Many Iranian companies do not simply need funding. They need reliability, tools, systems, verified suppliers, operational data, spare parts, logistics, and execution partners.

This is why the B2B layer matters.

Consumer demand tells us what households want.

Public markets show where price is visible.

Real assets show where capital seeks protection.

Scarcity shows where pressure is building.

Enterprise demand shows where the productive economy is forced to adapt.

That adaptation is where many investable opportunities begin.

Conclusion

Iran’s hidden B2B market is not hidden because demand is absent. It is hidden because the demand is operational, fragmented, local, and often buried inside the daily friction of doing business.

The opportunity is not simply to sell more products to companies. The opportunity is to solve the frictions that prevent companies from producing, moving, repairing, storing, measuring, sourcing, and delivering reliably.

Machinery maintenance, spare parts, procurement intelligence, energy reliability, water efficiency, logistics coordination, enterprise software, supplier verification, business services, and operational data all become important when the economy is difficult to run.

For investors, the lesson is direct: do not look only for sectors that are growing. Look for bottlenecks that companies cannot afford to ignore.

In Iran, some of the strongest B2B opportunities will appear not where the market looks smooth, but where the friction is most expensive.